On the first trading day, all heck breaks loose.

In China, stocks crashed on day one of 2016. No one really knows why. Some hardy souls blamed the manufacturing index that came in even lousier than in November. But manufacturing has been consistently lousy, and bad numbers are nothing new and not a reason for the sudden plunge in stocks.

Whatever the reasons, the Shanghai Composite plunged 6.9%, the Shenzhen Composite 8.2%. At that point, panicked authorities halted all trading via a circuit breaker announced in December. Everything is stuck. No one knows what any of these stocks are worth. Not exactly a confidence-inspiring move.

And in one single day, the indices blew a big part of their gains since the crash last summer. This rattled investors in other parts of Asia. The Japanese Nikkei dropped 3.1%, Hong Kong’s Hang Seng 2.7%.

Red ink instantly bled into Europe, covering all major indices. Among them, the German DAX was the biggest loser, down 4.3%. Germans in general are leery of the stock market and prefer to keep their money in the bank or plow it into real estate. But the DAX is the favorite playground for US mutual funds, ETFs, and hedge funds. And they’re suddenly getting cold feet in this happy New Year.

So this is what investors in the US woke up to, after having already been kicked around in 2015.

The promised and much ballyhooed, and often reliable Santa Rally lasted only three miserable low-volume days right before Christmas, after weeks of selling, and before getting destroyed entirely in the final days of the year. It left the US indices in the red for December, a bitter disappointment for Wall Street soothsayers that had screamed in unison since fall, buy buy buy the coming Santa Rally.

And now this: the Dow is down 410 points, or 2.3%, as I’m writing this. The S&P 500 is also down 2.3%, and the Nasdaq 2.8%. Barring a last-minute miracle rally, of the sort we’ve seen many times before, this is going to be an inauspicious beginning of the year.

It isn’t what folks have been hoping for after a year when the only thing that seemed to make money was shorting anything related to energy and commodities, going long the hated dollar, and loading up on the 10 mega caps that propped up the S&P 500. Without those 10 stocks, the S&P 500 would have been deeply in the red, rather than only slightly in the red.

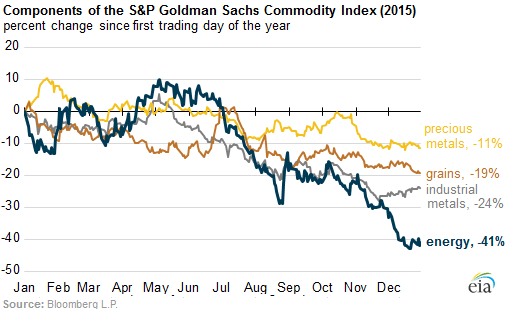

The entire commodities space got hammered last year. This chart from the EIA shows the bloodletting that transpired by sector in industrial metals, precious metals, grains, and energy:

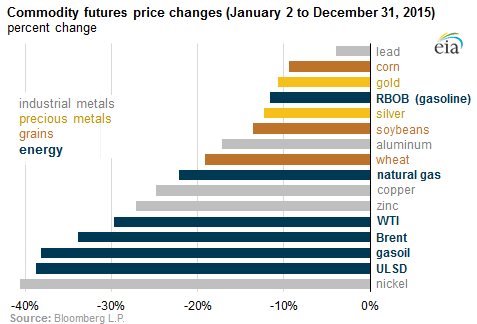

And this EIA chart shows the rout by individual commodity, color-coded by sector:

Today doesn’t look promising either so far, with the price of crude oil sinking. Even as the first tanker loaded with US crude left Corpus Christi to deliver the previously forbidden cargo to the world, WTI dropped 1.5% to $36.50 a barrel. The hoped-for salvation of the US oil sector might have to wait another day.

Everyone was looking forward to the New Year, when this great injustice would end, the injustice of markets doing things other than soaring, despite ongoing central-bank stimulus around the globe with zero-interest-rate and negative-interest-rate policies ruling the day, and with QE still flooding the Eurozone and Japan with freshly printed money.

The Economics and Strategy team at Canada’s National Bank put it this way in their BNF Economic Monitor:

Good riddance 2015. The global economy’s performance was the worst in six years despite a massive stimulus to consumers around the world courtesy of lower energy prices and highly stimulative monetary policy. As it turns out, those boosters were offset by headwinds generated by China’s rebalancing towards a more service-oriented economy which proved more challenging than first thought, particularly for trading partners in emerging economies. The bad news is that those headwinds will continue to restrain growth in 2016.

And now on the first trading day of this glorious year 2016, we get a morose data dump:

The Markit US Manufacturing PMI for December dropped to 51.1. Though still barely in expansion mode, it was the lowest since October 2012, on a “near-stagnation in new business volumes.” New orders grew at “the weakest pace since September 2009.” The report added these morsels:

Anecdotal evidence cited softer underlying demand conditions, intense competition for new work, and subdued business confidence among clients.

The manufacturing sector saw a disappointing end to 2015, and its plight looks set to continue into the New Year as headwinds show no sign of abating any time soon. Order book growth has stalled as producers report some of the toughest trading conditions since the end of the global Financial Crisis.

The ISM’s Manufacturing Report on Business for December is even gloomier. It dropped to 48.2, now in contraction mode for the second month in a row, with the sub-indices of New Orders, Inventories, and Production and Employment all contracting.

And in Canada, which spent 2015 flirting with more than just a technical recession, the RBC Manufacturing PMI offered some special treats this morning, as it dropped to 47.5 for December, in contraction mode for the fifth month in a row.

Ironically, Canada is supposed to be one of the beneficiaries of the strong dollar. The loonie has plunged 17% against the greenback in 2015, and earlier today hit $0.7152, a low not seen since 2004. The US is by far Canada’s largest export target, and exports of goods manufactured in Canada should boom. But no. The RBC PMI report:

The latest PMI reading was the lowest in just over five years of data collection, largely reflecting weaker contributions from the output, new orders, and employment components.

Business conditions in the Canadian manufacturing sector fell at a survey-record pace in December as weaker domestic demand and ongoing uncertainty in the energy sector continues to take its toll.

So this eagerly awaited year 2016, when all the market wrongs of 2015 would be rectified, and when central banks would once again be able to push markets higher with their scorched-earth monetary policies and their verbal manipulations, begins very inauspiciously with just a touch of mayhem.

But it’s not just manufacturing. It’s now dragging non-manufacturing into the mix, at least in the Midwest. Ugly, ugly, ugly. Read… Business in the Midwest Takes Worst Hit since July 2009

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Good afternoon Wolf:

My thoughts on the market…

Who do you take your political advice from? Investing advice?

Is your decision-making based on what everyone around you is doing or worse, from what the so-called ‘experts’ are telling you to do?

In other words are you a member of the sheeple class?

As this look back at history will show you, that may be the worst place to be!

I wrote this today: ‘Following The Herd Or Worse, The ‘Experts’, In Politics And Investing!’ (https://www.linkedin.com/pulse/following-herd-worse-experts-politics-investing-future-haltman?trk=prof-post)

Mike

Hahaha Mr Haltman have you heard of “reality”? Might want to check on that.

Fifty times valuations on stocks, bonds and real estate do to “cheap and easy” money handed to manipulators is not a true reflection of the US nore the worlds economy and financial stability!

Do not worry, fixed…

http://www.zerohedge.com/news/2016-01-04/close-market-ripple-which-stopped-stocks-tumbling-1101-am

The Dollar is recovering nicely.

Everything going down against the USD. Is that deflationary?

Not to worry, if things get bad the Fed can cut the interest rates and prosperity will resume.

Maybe Mr. Bubble just encountered Mr. Pin…

The blame for all this goes back to the USA printing far to much cheap cheap money for far far too long. And not much of it went to hard working people . most of the money went to the financial institutions and big bisness ..and most of it has been wasted .money must have a cost .ZIRP for far to long will have a terrible cost The Obama administration should be shot for damage they have aloud to happen not just to the us but to the world economy as well .

And, pray tell, exactly what has President Obama done to the economy? It’s the Federal Reserve that prints money and Congress (GOP these days) that spend it or give it away.

The election year is off to an impressive start.. Things might get rough out there as the economy faces up to some tough restructuring; but at least us voters have the new hope of –> insert candidate name here <– to look forward to!

Seriously though, if that's what is being planned it's not stupid. Unless things become uncontrollable like in 2008.

But with back stops to financial markets still being implicit, we needn't fear another collapse like the previous one. So What really worries me is the possibility that excessive nation state debt (which was in effect shifted there from private industry after 08) inflames National tensions as it becomes unserviceable. Mr. Wolf, do you think what happens in Greece could occur on a grander scale in 2016?

In that regard, I'm thinking of the book 'bad samaritans', which describes how the strategic use of tariffs can protect and help a poor country's economy develop. As the world enters recession and select developing nations full depressions, perhaps we'll see another rise in nationalism around the world in response to the unserviceable debt loads holding them down.

Too much Debt is a terrible 4 letter word when things go wrong .and the world is awash with it

If anyone is expecting demand to pickup in 2016, it won’t. Incomes are down significantly, rents are up, as are other expenses. The disposable income isn’t there to support higher prices. The markets are nowhere near the levels that reflect actual consumer spending.

Manufacturing employs only 9% of the US workforce and accounts for only 12% of the overall economy, which is otherwise driven by consumer spending and services.

The Regional Manufacturing Average (Empire State, Philadelphia, Richmond, Kansas City, Dallas) closed out the year at the worst level since the financial crisis in early 2008.

Virtually ALL global economic indices are a disaster and getting worse! Mix in the rapidly degrading global macro/political military posturing and you have a world situation that is historical in nature.

Gives new meaning to the ancient Chinese curse of; “May you live in interesting times”.

Disposable income is a strange number. Your health insurance payments are considered part of disposable income. My insurance went up 50% for the same coverage.

The way they figure disposable really, really needs an overhaul.

And meanwhile new car sales are up

With the Chinese economy in “transformation”, Europe still living with the euro crisis (southern Europe is bankrupt), Russia living under western imposed sanctions, and the U.S fracking industry which created an oil glut that crashed the oil price and took away the revenue from emerging markets… no one seems to have money to spend… exactly how is the global economy going to grow under these conditions ?

Is this it? Or will the Plunge Protection Team buy up futures to force the market back up?

Isn’t the first quarter usually positive with people adding to their 401k and pension funds? Or do we suppose that there isn’t much there to add?

And isn’t a year leading up to an election also usually positive for the markets?

I can come up with many scenarios of how the PTB could run this back up.. although they seemed to have tried for most of last year.. and were successful for the first half and then things just ran out of gas or positive effects from the last QE.

So as messed up this first day was, the only really clear vision is hind sight and we won’t have that until we finally are at the end of this experiment in financialization and manipulation.

What’s going on at the Fed on the repo,s 31 Dec 2015?

http://mobile.reuters.com/article/idUSKBN0UE18Q20151231

“The global economy’s performance was the worst in six years despite a massive stimulus to consumers around the world courtesy of lower energy prices and highly stimulative monetary policy.”

Nobody questions commodity prices are lower, but do they really translate into a “massive stimulus”? Really, how much? 2016 brought with it the usual flurry of price increases, which won’t add to CPI. And everybody knows the split second WTI and Brent are back at around $60/bbl, fuel prices will be the same of when they were $100/bbl.

And money’s cheap if you are a huge company or even more so if you are a government, but what about the rest? Credit isn’t exactly spilling into the real economy and generating a 2006-style boom.

Yes, I know: cars. But to be completely honest I am starting to question those fantastic figures. Number plates (which around here are tied to the vehicle, not the owner, and are consecutive and not customizable) tell a completely different story: sales rolled over and died before the Summer. Unless of course people buy cars just to keep them in their garages.

The good people Canada’s National Bank may want to hold to their hats: I do not know exactly what will happen in 2016, but of one thing I am certain. 2016 will see central banks and national governments doubling down on their efforts to “stimulate” their own economies.

They won’t succeed, unless they start calculating CPI’s honestly. In that case they will find they have far exceeded their 2% goal.

Until liquidation is allowed to happen we’ll have another rocky ride like 2015 was, with panics born from nothing and rallies born from even less. And official figures becoming so downright detached from reality as to give China a run for her money.

Now off for the big questions: will the BOJ first and the ECB later go full kamikaze mode and add stocks to their QE programs? The BOJ already buys equities and J-REITs. The ECB has already authorized member banks (remember: QE is not conducted directly from Frankfurt… nudge nudge, wink wink) to buy BBB- rated corporate bonds.

Will the FANG be able to hold on to its gains or will investors start cashing in their chips (holding valuable stocks is nice… but building a new swimming pool is much better)?

Will the dollar and the yuan, joined at the hip, continue to be the one-eyed kings in the land of the blind?

Will Sweden follow up recent threats and unleash her financial weapons of mass destruction?

Will the flood of Chinese buyers continue to prop up selected housing markets in Australia, the US and Canada? Or will extreme valuations be their own cure?

Will energy stocks finally get whacked over the head like it should have happened more than a year ago?

Stay tuned, same Bat-Time, same Bat-Channel.

Vehicle production is the last number to worry about- each one has a serial number and when purchased a registration. Tampering with either is criminal. The VINs all go to government,

Because you are an area where the license stays with the car-you aren’t in car mad North America. The US has more cars than drivers licenses- Canada not far behind ( per capita)

A strange and worrying feature here are the ‘cash- back’ car loans.

Yes you can actually walk out with the car, well, drive out, and a grand

or two. In the last month it was called ‘Christmas cash’

I pretty sure this is going to lead to some elder abuse as Granny ends up buying a car without wanting to.

However I agree that this is heading for a huge crash

Besides manufacturing news, only theory I liked was the chinese currency devaluation. It can cause interest rate spikes in the hibor abd shibor against the USD causing a credit crunch. Makes chinese stocks drop and it spreads.

Chinese have been quietly devaluing and just last week or two those rates started to spike, same thing happened last august.

China devalues. Causes credit crunch, stocks drop then it spreads.

But who knows, but I do need to read more on china to see if more devaluation is coming.

Wolf –

I would feel a lot better about the world economy if I heard one positive thing from anyone other than “US consumers are continuing to spend” (until they can’t any more) and US folks are buying cars (on a trillion dollars of borrowed money). Does anyone have anything positive to say about the world economy other than it’s not as bad as we thought it might be?

From BI today – “San Francisco Federal Reserve President John Williams said Monday he is unfazed by the weak economic data out of China that has spooked Wall Street, and sees three to five U.S. interest rate hikes this year as reasonable given the strength of the U.S. economy.” But he says nothing to justify his forecast. Why should anyone place credence in his comments. Is this just cheer leading?

The only folks who seem to think that securities will go up in 2016 are the folks that are peddling them. What’s wrong with this picture?

My question is serious. Does anyone see any significant positive indication of world economic growth? If so, I hope you will post your thoughts.

Great questions, Curious Cat.

My next article is about American Craft beer. It’s a huge boom, a great product, and a real success story. And I love to drink this stuff. So there’s is something that will make you feel better about the US economy, if only a tiny slice of it, and if only at the expense of the industrial brewers :-]

Cheers to that Wolf! I am enjoying some really good brews down here in New Zealand at the moment. If I had to choose a favorite, it would be “The Rogue Hop organic pilsner” from Harrington’s Breweries. Ummmm ummmm.

Cheers to craft beer makers, and screw the industrial brewers. Especially the InBev type cheap credit M&A queens. The downside of it is, the small brewers feel the need to bulk up and go into an acquisition spree, too.

As Wolf pointed out, there are always opportunities out there, some simple, some complex, some big, some small and so forth.

That said, you asked about global growth. I think that answer is “No”. The only out I see if is a large enough block of countries walks away from the current state of affairs, dumps their debt (a big middle finger to Western banks so to speak) and carry on amongst themselves. I suppose any other sort of debt jubilee would work, but don’t bet on that happening – every place is so corrupt they spend all their time skimming.

On the contrary, I think South East Asian countries with younger demographics will fare far better than those other SE Asian countries with older/aging demographics (all of the Western world is old and aging). Asians tend to have more discipline in education and family, as say compared to Africa or the Middle East, and are wealthier as a result. I don’t like the lack of common law though – a big negative to me.

The other major factor is that old people aren’t as productive and cost more than younger folks which consume more (families/etc) and on the whole are more productive. This is going to become a huge problem in the US as more folks age into the Medicare/Social Security system and there is a collapsing workforce picking up trash, driving trucks, running farm tractors, running businesses, and the like.

To all you older folks – I get it – you have experience and all that. But today I had to bust ice off my drive way with a big steel breaker bar as it didn’t fully melt from our last snow/rain and we had a serious cold front move in. Can’t drive up my drive way, even with winter tires. Five minutes of that reminds me that I am getting older – and can’t do the kind of work I used to do all day (e.g. digging post holes – and busting rocks in the bottom with a breaker bar).

I actively educate myself and seek opportunities that layer value on my skill set in a bid to stay employed. I can’t make it as a dumb plow mule anymore – and neither can you so don’t act it. There are jobs out there for smart plow mules, but they are certainly less in number than the count for dumb ones. And things are going down hill to boot.

Just how it is and my point.

Regards,

Cooter

After the last crash in August, China banned certain selling by large shareholders. That ban expires Friday. I think the Monday crash might have been just front running.

The way I see it, demand is slumping because who are living in a seemingly paradoxical world, where the vast majority of people is increasingly unable to afford necessities in life, yet for the stuff they can afford like phones and LED lamps, technology has improved the real world utility over cost ratio so much to the point that people see no real benefit beyond spending more than a minimal amount.