Moment of truth for over-indebted Corporate America.

Fed Chair Janet Yellen herself put a December rate hike back on the flip-flop table today. Instantly, the dollar regained additional strength. It has been rallying recently, after a rough summer when disappointing economic data hailed down on the land while the Fed flip-flopped on rate hikes. Now the theory goes that the dollar will continue to rally.

But not so fast, says a new report by Stéfane Marion and Krishen Rangasamy, economists at NBF Economics and Strategy. While the dollar may still have some upside “over the near term,” they write, it is “close to peaking.”

Numerous US companies have blamed their revenue and earnings debacles on the strong dollar. Revenues for the S&P 500 have been declining all year, a first since the Financial Crisis, and earnings are set to decline for the second quarter in a row.

US companies with global operations get hit by the strong dollar in two ways: exports come under pricing pressure and revenue and profits made in plunging foreign currencies end up on the income statement as stronger but fewer dollars.

Persistent revenue and earnings declines entail further “efficiencies,” so layoffs. We’re already getting bombarded with layoff announcements. What these companies need, after years of loading up on debt to buy back their own shares and acquire each other, is a lot of inflation and a weak dollar to make their debts appear sustainable.

The strong dollar is the moment of truth for over-indebted Corporate America. So the report:

As it turns out, earlier USD strength is proving to be more damaging to the economy than first thought. The strong greenback has not only restrained economic growth via slumping exports but also caused import prices to fall, both working to pull the inflation rate down.

Falling import prices and lower inflation are good for consumers but deadly for over-indebted Corporate America.

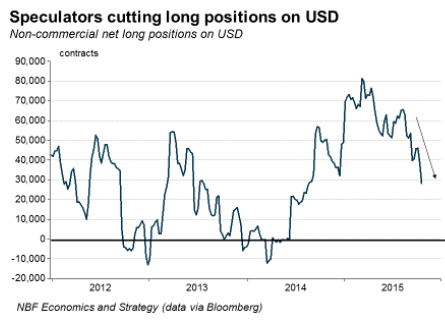

Betting on the strong dollar was the trade last year and early this year. But since then, currency speculators have been slashing their long positions in the dollar. And this too hammered the dollar over the summer:

By backing away from dollar long positions, speculators have joined the rest of Wall Street in doubting the Fed’s willingness to raise rates. And that may cause the Fed to put its foot down. The report:

The Fed already has a credibility problem ─ markets are pricing in far fewer rate hikes than the FOMC says it expects over the next couple of years ─ and it will do what it can to restore its credibility. That’s why we believe the Fed will set aside concerns about low inflation and raise the fed funds rate in December for the first time in almost a decade.

And since such hike is not fully priced in, the USD has potential for further gains over the near term.

But after the Fed’s show of tepid force or whatever, the dollar would face reality. Next year, the economy will likely face additional “headwinds.” The strong dollar would continue to drag on exports. Demand in the US “could also take a breather.” The housing market is “likely to soften.” And “consumption growth could ramp down as the benefits of low pump prices fade and employment creation moderates….”

So not exactly a rosy scenario. Hence, “the upcoming tightening cycle is set to be brief,” the report says. That would spell trouble for the dollar rally.

The other pressure building up against the dollar: The IMF is likely to include the Chinese yuan in the Special Drawing Rights, a currency basket that contains the dollar, the euro, the yen, and the UK pound.

Once the yuan is part of the SDR, central banks will add yuan to their reserves. But reserves have been falling since last year, and adding another currency to the falling total would come out of the hide other reserve currencies [read… Not the “Death of the Dollar” but “Death of the Euro?”].

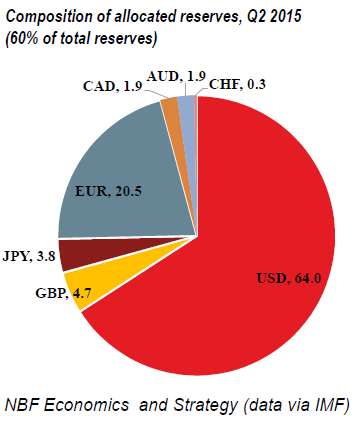

The dollar reigned supreme as a reserve currency in Q2, with a share of 64.0%, down a smidgen from 64.1% in Q1. The euro’s share dropped further to 20.5% in Q2, down from 20.7% in Q1, and from 27.6% at its peak in 2009 before the debt crisis revealed what it was made of:

So more demand for the yuan might let some hot air out of the dollar – at least that’s what everyone is hoping. It would “arguably lower downside risks to the global economy,” the report says, given the mountain of dollar-denominated debt issued recklessly by companies and governments outside the US that didn’t want to issue this debt in their own currencies because it would have borne higher interest rates. Now that these debt sinners’ own currencies have plunged against the dollar, the math no longer works.

A weaker dollar could help them out and, as the report says, “help reduce the odds of corporate default and capital outflows in emerging economies,” and it could help prop up the “stability of the world economy.”

From that point of view, and from the point of view of Corporate America, it’s clear why bashing the dollar – and along with it, the earnings power and wealth, if any, of every American – is the way to go. And beyond the near term, the dollar bashers will likely win.

And the biggest debt sinner of them all? The US. Gross national Debt, that monster that keeps ballooning so much faster than the infamously slo-mo economy, just did something phenomenal. Read… US Gross National Debt Jumps $340 Billion in One Day

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

It says an awful lot when the fate of the whole financial world hinges on the possibility of a 0.25% rate hike. And none of what it says is good.

Yes, it is only a .25% rate hike, but you forget that Human perception struggles with the non-linear. When rates are 10%, a 100 basis point move is only a 10% hike. When rates are 2%, a 100 basis move is 50% hike. So today with rates at 0 to .25% and 25 basis point move is a 250% to 100% hike! Sooooooo, when viewed this way,it is a big deal!

“What we see in China and Greece, along with untold others, are mere nodal points in a complex and fragile daisy chain – held together by

quadrillions of dollars in derivatives and ultimately promises backed by

faith.

The point is that small changes at these extremes can be dangerous. They can result is ripples that spread out much further than rationally

imagined.” The internet…

Cheers

Jeff

very few get what you say about the 25 basis point raise. Or understand what it will do to the derivative market. But then we are speculating as she won’t raise rates.

But, I thought everything was awesome?

This is good, but it does take a bit of time to work through:

http://www.zerohedge.com/news/2015-11-04/how-global-debt-bubble-crushing-global-commodity-prices

But any set back will be a short one, or so I’m told. So not to worry. All is well. So march right out there and buy some stuff. Run up those credit cards. We need a show of strong 1st Class American Consumerism here.

So, get on out there and spend with confidence. I’ll be right behind you. Trust me. Right behind you. Soon. Don’t wait on me though. Just go on out there and make this economy work!

The RE bubble is seriously popping back home in Canada, I look forward to picking up some discounted properties with the strong USD. It’s not all bad.

It’s not a pop until the people of Toronto and Vancouver get burned in housing. I’m really looking forward to that.

Yea, I wouldn’t hold my breath for Vancouver, they seem to exist in another universe.

That’s right, Night Train. Absolutely nothing to worry about, why the economy is TITANIC! No wait that’s not right…it’s ready to erupt like Vesuvius…no, that didn’t end well, um…wait I know we can grow sunflowers in North Dakota…ah, that won’t work…let’s move to NYC and open an account at CITIBANK and buy STOCKS…um, er, I here Nieman-Marcus is having a big sale! Hey, Petunia, want to go shopping with me and Night Train so we can boost the economy? Maybe we can get some True Religion jeans before THEY move to the Honduras? Oh, the possibilities are endless!

Julian, as the resident fashionista, I have the November issue of my favorite fashion magazine firmly in hand. The lack of good stuff to drool over is truly astonishing. Normally the holiday issues are as thick as a phone book, not this year. Less advertising, and wonder of wonders, more “less expensive stuff (very relative term)”. I am always available for an afternoon of power browsing at NM.

How about the other, more real-world measure of economic health: capital expenditures?? If it’s in the toilet with ZIRP, how will it get better at 0.25%? Corporate execs are the Kings Of Excuses and now that the borrowing binge is maxed out they will have to rely on actually trying to GROW their business or hope the Fed has their backs with more free money. Which scenario would you bet on?

I no longer believe they will raise rates any time soon, but if I’m wrong what I am certain of is that it will not be much long after that where we’ll see a total about-face as they leave skid-marks to implement QE infinity.

By, I assume, more ZIRP/QE and maybe NIRP/QE etc, Forcing Companies/People/Pension funds/states/countries etc. out on the risk curve.

So;

1. Companies can invest but mostly continue buying their own shares back, all by staying or going even deeper into debt.

2. Or the US consumer must start to consume again on credit as if there is no tomorrow based on falling real wages/incomes.

3. The 51 states their municipalities and The central government of the USA must start to spend as if there is no tomorrow all based off course on borrow money (more debt).

4. Or the rest of the world must start to spend as if there is no tomorrow all based off course on borrowing more USD (USD debt) (The USD is already 64 pct of all foreign banks reserves. The Yuan maybe becomes reserve currency. EU + JAPAN + UK also like to be a bit reserve currency.)

And by doing so they are creating new USD into circulation which are desperately needed by companies to pay off debt. After which a new cycle of stock buy backs can start and M&A ? Which need to be followed again by bringing down the interest rate to force number the above groups 1,2,3 and 4 to borrow and spend to make the companies pay their debt. Rinse and repeat. Soon we are at minus 25 pct on deposit account.

So the rest of the world besides the US companies must NOW go into debt to make it able to fore example Mr. Buffet pay off his purchase of Heinz with debt. Besides that the USD foreign reserve on the balance sheet of the central banks have to growth even further while China clearly have stated to become part of this reserve system.

If the world economy growths, and there are relatively less USD in circulation to a bigger world GDP, as a result of the YUAN becoming also world reserve currency, the value of the USD have to rise.

Besides that are reserves not there to be used one day ?? or are the usd reserves on the central bank balance sheets their only to become bigger and bigger ?

Or do I miss something ?

Death of cash.

How about making interest illegal?

When is the next Jubilee year?

(I see that a part of my text was not copied/pasted. so here one more time)

So if I understand it all well.

American companies are in debt, so we need inflation to make the debt load payable. So Yellen needs to bring the USD down.

By, I assume, more ZIRP/QE and maybe NIRP/QE etc, Forcing Companies/People/Pension funds/states/countries etc. out on the risk curve.

So;

1. Companies can invest but mostly continue buying their own shares back, all by staying or going even deeper into debt.

2. Or the US consumer must start to consume again on credit as if there is no tomorrow based on falling real wages/incomes.

3. The 51 states their municipalities and The central government of the USA must start to spend as if there is no tomorrow all based off course on borrow money (more debt).

4. Or the rest of the world must start to spend as if there is no tomorrow all based off course on borrowing more USD (USD debt) (The USD is already 64 pct of all foreign banks reserves. The Yuan maybe becomes reserve currency. EU + JAPAN + UK also like to be a bit reserve currency.)

And by doing so they are creating new USD into circulation which are desperately needed by companies to pay off debt. After which a new cycle of stock buy backs can start and M&A ? Which need to be followed again by bringing down the interest rate to force number the above groups 1,2,3 and 4 to borrow and spend to make the companies pay their debt. Rinse and repeat. Soon we are at minus 25 pct on deposit account.

So the rest of the world besides the US companies must NOW go into debt to make it able to fore example Mr. Buffet pay off his purchase of Heinz with debt. Besides that the USD foreign reserve on the balance sheet of the central banks have to growth even further while China clearly have stated to become part of this reserve system.

If the world economy growths, and there are relatively less USD in circulation to a bigger world GDP, as a result of the YUAN becoming also world reserve currency, the value of the USD have to rise.

Besides that are reserves not there to be used one day ?? or are the usd reserves on the central bank balance sheets their only to become bigger and bigger ?

Or do I miss something ?

We’re in new territory, globally. Spending is not the answer. The huge global corporations can’t survive what their greed has brought. It always comes back to reality. Maybe we’ll like the changes! Consider how much less stressful life will be without much government. Consider how much more prosperous we’ll be when that 64% tax rate fades as the structures slowly close down without money. So much more will be possible without all the endless regulation and permissions, not to mention harassment. Bring it on!

I read so many articles about how the US Dollar is going to crash.

I cannot see this occurring in the short to medium term.

US Dollar is the world reserve currency.

Any individual or company and even government believing that their country may have an economic or financial crisis will opt to exchange their local currency for the US Dollar.

On top of this the second most used currency, the Euro looks very fragile in the future.

Dollar is “crashing” (as some say) and “dollar bashing” (as in the article) are two different things. No one in the article thinks the dollar is going to crash. They’re saying the dollar is likely to peak soon and decline afterwards (not crash).

“The IMF is likely to include the Chinese yuan in the Special Drawing Rights, a currency basket that contains the dollar, the euro, the yen, and the UK pound”

how many of those currencies have a peg to the dollar?

how can a currency that is pegged to another currency in the basket be included in that very same basket of currencies?

isn’t that circular logic?

has this even happened before…..where a currency that derives it’s value from another currency in the basket be included in the SDR basket?

why does the fact that China printed trillions and trillions of Yuan not seem to matter for it’s inclusion in said basket? it’s total debt to GDP is 282%….and this is the best part, it’s been appreciating along with the dollar even though they have printed all that currency.

the mind boggles.

Yes “the mind boggles,” as you say :-)

For the IMF and central banks, a currency only has to be convertible. It’s not a big issue if a currency is pegged. The CHF was pegged too for a while, no problem. Many currencies are. But convertibility is the real requirement. No one wants to get stuck with a non-convertible currency.

“So more demand for the yuan might let some hot air out of the dollar”

which would also let some air out of the Yuan due to the peg…no?

The dollar going out of circulation world-wide is not the ‘dollar crashing’ it is the exact opposite.

As world trade declines — particularly the petroleum trade — there will be fewer dollars in circulation.

That makes each one of them more desirable with the unit ‘cost’ (in other currencies) rising. At the same time, dollars are used to retire dollar debt which means an increasing dollar shortage. (Dollars are ‘loaned into existence’ so they are ‘extinguished as they are repaid’.)

None of this says ‘dollar crashing’. Instead, it says ‘dollar scarcity’.

You write “What these companies need…is a lot of inflation and a weak dollar to make their debts appear sustainable.”

This is where I become confused. According to some, such as shadowfacts.com and even some previous posts here, actual inflation is closer to 10%.

So how does that figure into the equation?

whatever real inflation is, for these over-indebted companies, it’s not big enough.

I think the real problem is that the inflation target is set to low bringing down interest rates which has stalled wages .massive asset inflation all means less consumerism .A zero sum game. You have to pay desent wages with reasonable time off for rest and recreation to boast growth. Centralization policy is not good in the long run as you lose efficiency as costs skyrocket out of control

…. and yet everyone believes non of this is nefarious in nature. No one is attacking your life and ability to live it or your retirement. What ever solution that is offered is in our best interest.

This is too conspiratorial to be something we can all discuss..

Good comments, Wolf. Not realized by many ordinary folks, Reserve Currencies come and go. The first world reserve currency was the Portuguese escudo (for 90 years) and then came the Spanish peso (110), followed by the Dutch guilder (80) and then French franc (95) and the British pound sterling (105). The average was 96 years.

The US dollar as a reserve currency started at Bretton Woods in 1944 and that was 71 years ago based on Gold at US$35 a oz. But if the nuance escapes anyone, Nixon closed the gold window on August 15 1971 and now the dollar is backed by nothing but thin air.

Will the US dollar, as a world reserve currency, not go the same way as the 5 predecessors? Don’t hold your breath.

Since Robert Rubin’s reign in the Bill Clinton years the US exhortations have always been about maintaining a fake ‘strong dollar policy’.

That way the US could continue to have a free lunch and live beyond its means by huge borrowings via US Treasuries.

How to orchestrate a strong dollar index myth? Easy. Suppress the price of gold because it moves in opposite direction to the fiat dollar.

According to Paul Craig Roberts and Dave Kranzler: ” Comex futures trade 23 hours a day via a global computerized trading system known as Globex. The heaviest period of trading occurs when the actual Comex floor operations are open, which is 8:20 a.m. to 1:30 p.m. EST. All other times Comex futures trade electronically via Globex. Gold and silver are smashed primarily during the Globex-only trading periods, when volume is often light to non-existent.”

That happened in Oct before the trading started at the Shanghai Gold Exchange. A huge sale in paper gold in the US took place and the price of gold swooned.

The motivation of such large tonnage of paper gold sale during the low trading period is to press the price of Gold down and prop up the US dollar.

Roberts and Kransler said “One entity that can afford to use capital like this is the Federal Reserve, because the Fed can create its own capital for free using the printing press.”

Is the FED as “federal” as Federal Express? Yes.

https://biblicisminstitute.wordpress.com/2014/08/24/the-corrupt-federal-reserve-is-not-federal/