The infamous “sanction spiral” imposed on Russia by the US and Europe with such fanfare last year in the wake of the Ukrainian fiasco has receded from Western headlines. In Russia, it coagulated with the oil price plunge, and during the first two quarters this year, the economy shrank sharply.

But whatever the “sanction spiral” was supposed to accomplish, some countries in Europe, among them Germany, are desperately dependent on Russian gas to heat homes and offices, and to supply power plants and industrial installation. The threat that Russia would turn off the valve hung over the EU last winter. At the time, Eurocrats beat the bushes to explain that no one would be without natural gas. But not everyone believed it, including the German government [LEAKED: What Happens to Germany if Russia Turns off the Gas].

The scare seems to have left a lasting impression.

Or was it just about money?

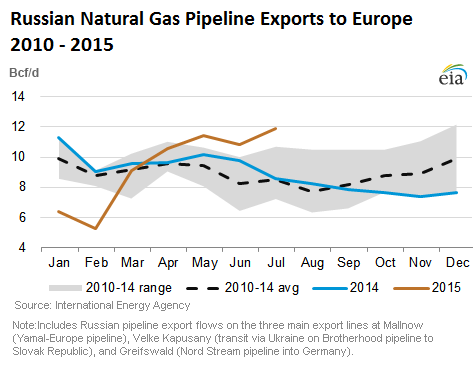

Over the winter, Russian natural gas exports by pipeline to Europe dropped to the lowest levels in years, and were 22% below the five-year average, according to US EIA calculations of International Energy Agency data. Exports dropped even further to 6.4 billion cubic feet per day (Bcf/d) in January and 5.3 Bcf/d in February, down 36% and 40% respectively from the five-year average for these months.

But in March, natural gas exports from Russia to Europe began to increase. And by the second quarter, they jumped 58% over the first quarter. In July, the most recent month for which data is available, exports hit 11.9 Bcf/d. Exports via the Ukraine decreased, but exports via the Nord Stream pipeline into Germany soared 55% year-over-year in June and 59% in July to a new record. To heck with any half-forgotten sanctions (2015 exports, brown line):

Then there’s the money.

During the first three months this year, the price averaged $9.36 per Million British Thermal Units (MMBtu). Then they began to decline. By August, prices had plunged nearly 30% to $6.66 /MMBtu, the lowest since 2009.

OK, those low prices might still look paradisiacal to US shale gas drillers. On the NYMEX, natural gas currently trades for $2.62/MMBtu. In hubs where production from the Marcellus – the largest natural gas producing region in the US – is sold, such as at Tennessee’s Zone 4 Marcellus hub, prices are barely above $1/MMBtu. This price collapse has haunted drillers since 2009. Now Wall Street is finally pulling the plug, and two major US natural gas drillers have already gone bankrupt this year.

Gazprom and other producers in Russia have suffered from the price plunge in their markets, but not like US shale gas drillers. In Europe, many contractual rates are linked to the price of North Sea Brent crude oil, which started plunging over a year ago. After a lag of three to nine months, the lower crude oil prices are pushing down natural gas prices.

So what’s the reason behind last winter’s sharp drop of natural gas exports from Russia to Europe? The sanctions? Russia’s counter sanctions? The fiasco in the Ukraine? Nope. Just money.

Shrewd European buyers.

These buyers took advantage of the situation, which is what traders do by definition. According to the EIA, they tried to “optimize their oil-indexed contracts by decreasing imports in the winter while drawing heavily on gas in storage in anticipation of lower natural gas prices in the spring and summer 2015.” They knew natural gas prices would have to follow crude oil prices with that three-to-nine-month lag.

After the winter drawdown of their natural gas inventories, buyers then took advantage of the lower prices in the spring and summer, went on a buying binge, and accelerated refilling their storage facilities, injecting a record 1,834 Bcf from April 1 through September 22. Storage levels have reached 2,578 Bcf, according to Gas Infrastructure Europe. Driven by the current low prices, they may set a new record by the time the injection season ends.

This strategy provides Europe with relatively cheap natural gas for now. But it doesn’t lessen at all Europe’s desperate energy dependence on Russia, and Russia’s equally desperate dependence on the European market.

Whatever Russia and China are trying to hash out will take years to build. And Europe’s efforts to find alternative sources of cheap natural gas are not always going in the right direction: for example, production at the Netherlands Groningen field was further limited by the government after drilling-related earthquakes frazzled the population. So the Russian-European energy marriage may be rocky and unpleasant at times, but opportunities abound, and neither side can afford a divorce even if they wanted to.

Natural gas in the US follows its own dynamics, those of Wall Street engineering. Read… A Spinoff Goes to Heck, after Just 10 Months

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

When watching European football, it is amazing how many stadiums have Gazprom sponsorship logos and advertising. This must cost quite a bit, and what the benefit is to Gazprom? Are there other nat gas suppliers that Gazprom competes with?

Gazprom are actually the official sponsor of the Champions League, as well as an official partner of FIFA for the 2018 world cup in Russia, which is why they are painted across stadia in Europe. What benefit Gazprom gets from these sponsorships is anybody’s guess – they probably thought getting their name out there would give them some nice PR, though judging by the negative reaction to their involvement, it hasnt quite worked.

Norway and UK produce meaningful quantities of nat gas but their cost base is relatively high. Momentarily there is no real substitution for russian pipeline gas. Nat gas from Russia is presently not subject to any sanctions. Hence the title of the article is misleading. The US wants Quatar to build a gas pipeline to Turkey crossing Syria which is likely the mean reason for the proxy war in Syria and the “birth” of the Islamic State.

This is a conspiracy canard. The major beneficiary of a Persian Gulf to Europe pipeline would be Iran which has immense gas reserves under gulf waters but no way to export them. Qatar has LNG facilities to export their gas and with no population to speak of and immense financial reserves no great need to boost exports. How many Ferraris and mansions does the al Thani family need?

Cyprus has large gas fields off its coast that are quite a bit closer to Europe and would only have to cross Turkey but to develop them requires the Greek Cypriots to reach an accord with Turkish Cypriots on revenue sharing.

Israel is already producing offshore natural gas and Egypt just announced a major gas find off their coast. There is no shortage of natural gas in the world just a delivery problem and pipelines are a lot more vulnerable to terrorist attacks than LNG tankers. Putting a pipeline across Syria, Iraq or even Turkey given the Kurdish problem seems pie in the sky in the near term.

Exactly!

Always remember two things.

First: football is a religion in most of Europe. Being associated with it is a huge image boost for anybody who can afford it.

Second: Gazprom is more of a political entity than a mere cash cow for the Kremlin, like Rosfnet and Rosoboronexport are. It’s effectively a (very important) branch of the Russian government and as such it engages in activities that would have even the largest Japanese keiretsu and Chinese State-owned conglomerates raise an eyebrow or two.

Mr Richter makes a very crucial point: Europe desperately needs Russian commodities as much as Russia desperately needs European “hard” currency.

There’s no way around it, whether the Cold War mummies at NATO and the hawks at the US Department of State like it or not.

Replacing Russian commodities and goods with those originating from more politically acceptable States could prove not just immensely expensive, but impossible as well. I am sure China would be absolutely delighted to supply Europe with large diameter steel pipes (ironically used to build, among other things, pipelines), but that would open a whole new can of worms, as Chinese steel exports are under close scrutiny due to well known dumping practices.

I know a company producing surgical instruments, and the bulk of their contractors is located in Russia. They tried differentiating (chiefly due to fear sanctions could be extended to their sector) but the Indian contractors they turned to to obtain samples could not match Russian quality and prices, when all was said and done, were the same if not higher. Sure, they could turn to Swiss or Japanese contractors, whose quality is on par if not superior to the Russians’, but prices are far superior.

In a more perfect world, one could simply justify a 10-20% price increase by mentioning “we are now using contractors from Japan and Switzerland instead of Russia”, but things do not work that way. Money always wins.

Very interesting article.

Market pricing dynamics at work in spite of political restraints. This analysis is not found in other news sources – at least by me.

Africa holds the key for huge future nat gas production.

Recent huge gas discoveries near Europe.

Egypt, Israel.

If the EU wasnt so racist and anti Israeli there would be no gas problem.

Now they have Egypt I am sure france will work out something with its muslim friends, as the Quatart pipe dream through Syria is looking more and more like just that.

The whole natural gas consumption in Europe dropped for 4 years by 22% – which is actually the share of the Russian gas as well. So, nothing should happen if “Russia would turn off the valve hung over the EU”. Otherwise Russia would do it.