Homeownership is the crux of a healthy housing market. But it’s on decline in America.

The largest private equity firms along with REITs and other institutional Wall-Street funded investors have piled into the housing market to gobble up vacant homes that first-time buyers and others could have, and would have, eventually bought for a reasonable price.

The Fed laid out the roadmap for these institutional investors: borrow money for nearly free, buy up hundreds of thousands of vacant homes across the country, drive up prices via the multiplier effect [How Wall Street Manipulates The Buy-to-Rent Housing Racket], which would bail out the banks that owned these vacant homes, then rent them out if possible, and sell rent-backed structured synthetic securities to yield-desperate investors and retirement funds and shuffle the risk and future losses off to them.

It worked. The entire chain. And everyone is happy with the Fed’s handiwork. So what if first-time buyers and many others can no longer afford to buy homes in many cities around the country as America is gradually converting to a country of renters.

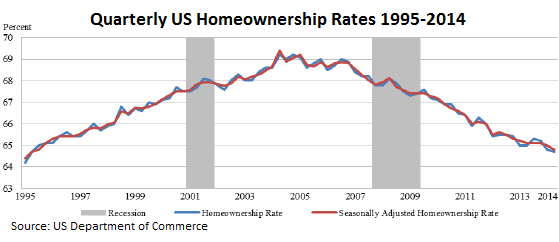

So in the second quarter, homeownership continued its inexorable downward progression, according to the Commerce Department. Seasonally adjusted, the rate dropped to 64.8% from 65.0%, the lowest since Q3 1995 (not seasonally adjusted, the rate dropped to 64.7%, the lowest since Q2 1995).

This is what the relentless trend looks like:

Homeownership since 2008 dropped across all age groups. But the largest drops occurred in the youngest age groups. In the under-35 age group, where first-time buyers are typically concentrated, home ownership has plunged from 41.3% in 2008 to 35.9%; and in the 35-44 age group, from 66.7% to 60.2%.

But the peak of ownership didn’t occur at the peak of the last housing bubble, or just before the financial crisis, but in 2004 when it reached 69.2%. Already during the early stages of the housing bubble, speculative buying drove prices beyond the reach of many normal buyers unless they wanted to resort to liar loans, which was a solution many chose. So the irony is not lost on us that homeownership started hitting the skids when “homes” became a risky, highly leveraged asset class to be flipped and laddered by speculators of all kinds, rather than be lived in by normal folks.

In San Francisco, where only about 36% of the homes are occupied by their owners – the rest are occupied by renters – home prices hit a slick $1,000,000, while soaring office rents blow up enterprises with real business models. It’s crazy. It’s powered by hot money from around the world. Then comes the moment when the hot money evaporates. Read…. How the Surge of Hot Money Pushes San Francisco to the Brink

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()